Profit and Loss Account is one of the elements of the financial statement and constitutes a summary of revenues and the related costs, as well as the financial results from the entire activity of the economic entity in a given reporting period.

In the profit and loss account, the presented revenues and costs are grouped according to the type of activity to which they relate: operating activity (core and other) and financial activity.

Core operating activity constitutes the main business activity of a given enterprise and may include production, trading, or service activities. Here, revenues from the sale of products (i.e., goods, works, and services), materials, and merchandise, as well as operating costs, are taken into account.

Other operating activity is indirectly related to the main activity (it may include, for example, social activities, sale of unnecessary fixed assets, giving and receiving donations). Revenues and costs related to this type of activity are called, respectively, other operating revenues and other operating costs.

Financial activity, which is associated with the generation of financial revenues and costs, concerns taking out loans and credits, granting loans, receiving dividends from owned shares and stocks, conducting securities transactions, and maintaining funds in bank deposits.

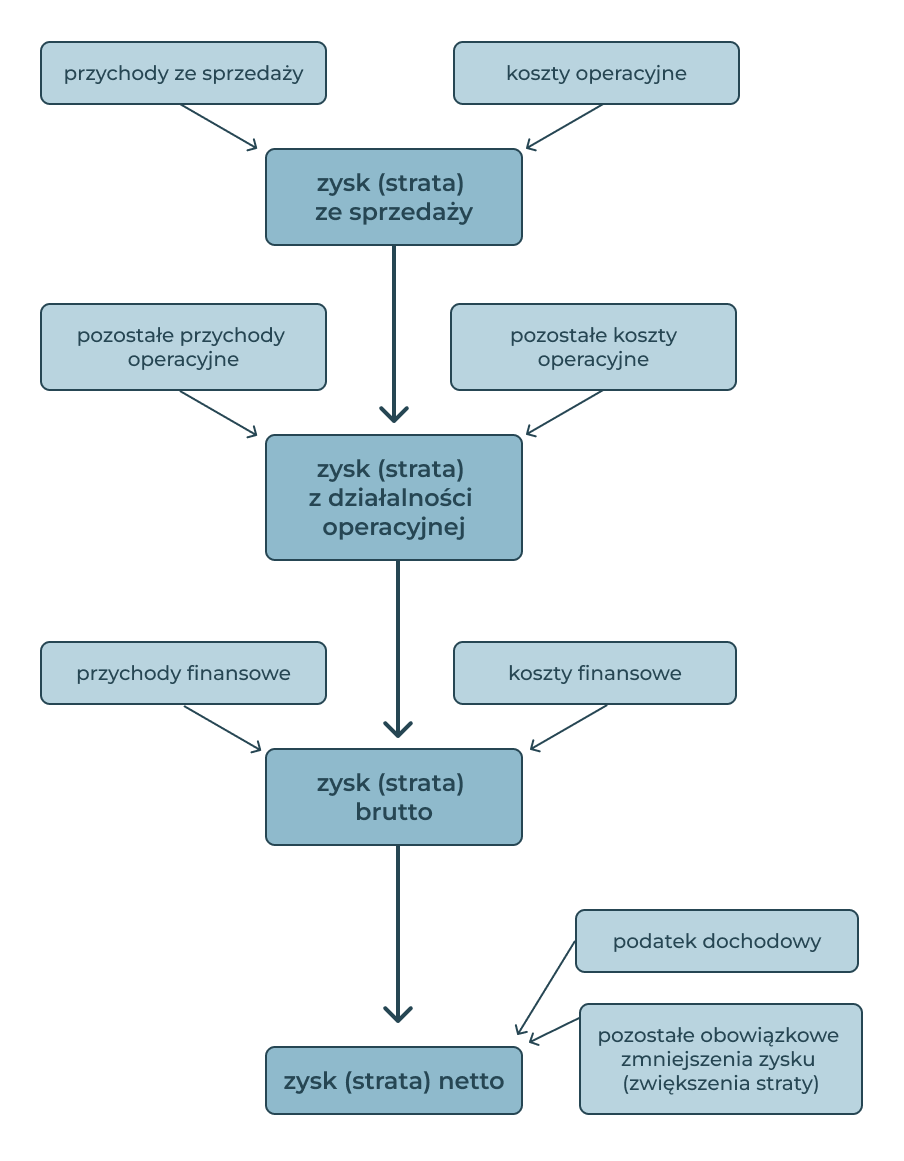

The purpose of preparing the profit and loss account is to determine the final financial result from the entire

activity, which is the net profit or loss. This final financial result is determined in a segmented manner (see Fig.

1). First—by comparing net revenues from sales of products, materials, and goods with operating costs—the result

from sales is determined. After adding to the sales result the other operating revenues and subtracting from it

the other operating costs, the operating activity result is obtained. This result, increased by financial revenues

and decreased by financial costs, ultimately forms the gross profit or loss. Then, after taking into

account income tax and other obligatory charges on the gross financial result, the net profit (loss) is

obtained.

The profit and loss account can be prepared in the comparative variant or the calculation variant. The choice of one of them belongs to the management of the economic entity. The templates of the profit and loss account in the comparative and calculation variants are provided in Annex No. 1 to the Accounting Act [1] (see tab. (1)).

The comparative and calculation variants differ in the way of recognizing costs from the core operating activity (see the upper and lower part of tab. (1)). In the comparative variant, costs are itemized according to their type (e.g., depreciation, wages), whereas in the calculation variant—according to the place of cost origin (e.g., cost of production of sold products, selling costs). When calculating the result from sales, in both variants we will of course obtain the same amount.

|

Calculation Variant |

Comparative Variant |

|

A. Net revenues from sales of products, goods, and materials |

A. Net revenues from sales and equivalent revenues |

|

I. Net revenues from sales of products |

I. Net revenues from sales of products |

|

II. Net revenues from sales of goods and materials |

II. Change in products inventory (increase – positive value, decrease – negative value) |

|

B. Costs of sold products, goods, and materials |

III. Cost of products produced for own needs |

|

I. Cost of production of sold products |

IV. Net revenues from sales of goods and materials |

|

II. Value of sold goods and materials |

B. Operating activity costs |

|

C. Gross profit (loss) from sales (A–B) |

I. Depreciation |

|

D. Selling costs |

II. Consumption of materials and energy |

|

E. General management costs |

III. External services |

|

F. Profit (loss) from sales (C–D–E) |

IV. Taxes and charges |

|

|

V. Wages |

|

|

VI. Social security and other benefits |

|

|

VII. Other type costs |

|

|

VIII. Value of sold goods and materials |

|

|

C. Profit (loss) from sales (A–B) |

|

G. Other operating revenues |

D. Other operating revenues |

|

I. Profit from disposal of non-financial fixed assets |

I. Profit from disposal of non-financial fixed assets |

|

II. Grants |

II. Grants |

|

III. Revaluation of non-financial assets |

III. Revaluation of non-financial assets |

|

IV. Other operating revenues |

IV. Other operating revenues |

|

H. Other operating costs |

E. Other operating costs |

|

I. Loss from disposal of non-financial fixed assets |

I. Loss from disposal of non-financial fixed assets |

|

II. Revaluation of non-financial assets |

II. Revaluation of non-financial assets |

|

III. Other operating costs |

III. Other operating costs |

|

I. Profit (loss) from operating activities (F+G–H) |

F. Profit (loss) from operating activities (C+D–E) |

|

J. Financial revenues |

G. Financial revenues |

|

I. Dividends and shares in profits |

I. Dividends and shares in profits |

|

II. Interest |

II. Interest |

|

III. Profit from disposal of financial assets |

III. Profit from disposal of financial assets |

|

IV. Revaluation of financial assets |

IV. Revaluation of financial assets |

|

V. Others |

V. Others |

|

K. Financial costs |

H. Financial costs |

|

I. Interest |

I. Interest |

|

II. Loss from disposal of financial assets |

II. Loss from disposal of financial assets |

|

III. Revaluation of financial assets |

III. Revaluation of financial assets |

|

IV. Others |

IV. Others |

|

L. Gross profit (loss) (I+J–K) |

I. Gross profit (loss) (F+G–H) |

|

M. Income tax |

J. Income tax |

|

N. Other obligatory decreases in profit (increases in loss) |

K. Other obligatory decreases in profit (increases in loss) |

|

O. Net profit (loss) (L–M–N) |

L. Net profit (loss) (I–J–K) |

Ustawa z dnia 29 września 1994 r. o rachunkowości Dz.U. 1994 nr 121 poz. 591 z późn. zm. url: https://isap.sejm.gov.pl/isap.nsf/DocDetails.xsp?id=WDU19941210591. (accessed: 13.03.2023).